EV Charging Point Operators (CPO’s) Market in India

EV Charging Point Operators (CPOs) Market in India: State-wise Opportunity Mapping, Unit Economics, and Competitive Landscape.

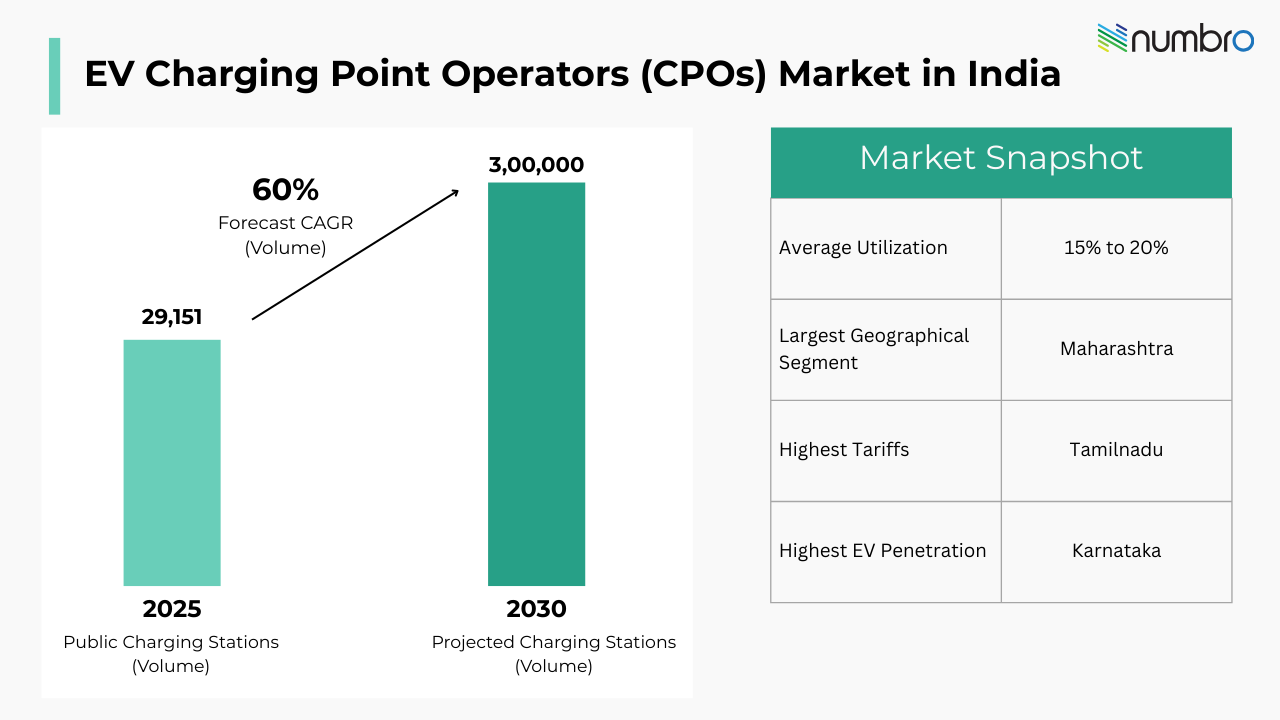

EV Charging Point Operators Market In India

EV charging infrastructure refers to public and semi-public charging stations that supply electric energy to electric vehicles across urban, semi-urban, and highway environments. The market includes AC chargers, DC fast chargers, ultra-fast chargers, and associated energy management systems deployed across city clusters, fleet hubs, and intercity corridors.

The India EV charging point operators market has expanded rapidly between 2022 and 2025 and is now transitioning from installation-led growth to utilisation-driven expansion. Market performance is influenced by EV penetration levels, state-level policies, grid readiness, tariff structures, corridor electrification mandates, and fleet integration trends.

Largest & Fastest Growing Segments

DC fast charging forms the core of the market, emerging as the dominant revenue driver due to its alignment with higher-power and high-utilisation use cases. Demand is primarily concentrated in four-wheelers and commercial vehicles, as these segments generate significantly greater energy throughput compared to smaller personal mobility categories. Market value remains clustered in leading EV-adoption states, reflecting stronger policy continuity, urban density, and fleet presence, while CCS2 has established itself as the prevailing connector standard across fast-charging infrastructure.

Looking ahead, growth momentum is increasingly shaped by the continued expansion of fast-charging networks, the rising contribution of emerging states beyond traditional leaders, the scaling of commercial and fleet-based applications, and the ongoing consolidation toward globally standardised connector technologies.

Market Dynamics

The India EV charging infrastructure market is supported by rising EV adoption, strong policy backing, corridor electrification mandates, and expanding fleet usage across logistics and public transport. However, moderate utilisation levels, grid constraints, tariff variation across states, and high capital costs for fast-charging infrastructure continue to impact site viability. The industry is gradually shifting from rapid installation growth toward utilisation-driven expansion, with increasing emphasis on corridor deployment, fleet integration, and unit-level economic sustainability. corridor classification (immediate, growth, white-space), and technology integration (CMS, smart charging, solar integration, battery swapping, ultra-high-power and bidirectional systems).

Market Segmentation

The India EV charging infrastructure market is segmented by charging type (AC, DC fast, ultra-fast), vehicle segment (2W, 3W, 4W, commercial/fleet), connector type (CCS2, Type-2 AC, Bharat DC-001, CHAdeMO), geography (state-level analysis),

Regional / State Analysis

Charging deployment is concentrated in a limited number of states, with significant disparity in charger density and EV-per-charger ratios across regions. Leading states show higher infrastructure maturity, while several states remain underpenetrated, indicating expansion opportunities over the forecast period.

Investment Landscape

The sector experienced peak funding during 2022–2023 followed by capital normalisation. Investment focus is shifting from rapid infrastructure expansion toward utilisation efficiency, revenue per charger, and state-level economic viability.

Key Questions Addressed by the Report

- What is the projected growth trajectory of India’s EV charging infrastructure market through 2030?

- How will revenue growth compare with charging point expansion over the forecast period?

- Which charging types are expected to generate the highest market value?

- Which vehicle segments will drive the majority of charging demand by value?

- How concentrated is market share across leading states, and which regions offer emerging growth potential?

- Where do state-level supply and demand gaps exist based on EV-to-charger ratios and charging density?

- How will highway expansion and corridor electrification influence deployment patterns?

- What factors determine site-level profitability, including utilisation, grid access, and vehicle mix?

- How does variation in state electricity tariffs impact charging economics and return profiles?

- What is the evolving competitive and investment landscape, and how is capital allocation shifting within the industry?